The geopolitical shifts of recent years have created a new reality for European industry. It has become clear, at the latest since Russia’s invasion of Ukraine in February 2022, that technological sovereignty is not merely an economic imperative but an increasingly existential question of national security. Germany’s Zeitenwende marked a historic turning point in its security policy: from a country that had systematically invested in the peace dividend for decades to a nation on course to reach defence spending of 3.5 % of GDP by 2029.1

1 Business Sweden (2025): Germany’s record defence modernisation drive. Oktober 2025. Online: https://www.business-sweden.com

The 2026 defence budget illustrates the scale of this transformation: Germany has approved a defence budget of €108.2 billion for 2026 – more than double the 2022 figure and, for the first time, surpassing the United Kingdom as the NATO member with the highest absolute defence expenditure in Europe.2 3 Simultaneously, all 32 NATO members have met the 2 % of GDP target for the first time since the Alliance’s founding – a paradigm shift that is fundamentally transforming not only state budgets but Europe’s entire technology and innovation ecosystem.4 5

2 AtlasInstitute for International Affairs (2025): Germany’s Path to Kriegstüchtigkeit: The 2026 Defence Budget. Dezember 2025. Online: https://atlasinstitute.org

3 Federal Ministry of Defence (2025): Defence Budget 2025 and 2026. Available at: https://www.bmvg.de

4 NATO (2025): Defence Expenditure of NATO Countries (2014 -2025). Pressemitteilung Juni 2025. Online: https://www.nato.int

5 Bird & Bird LLP (2026): Defence Spending in 2026. Online: https://www.twobirds.com

What is often overlooked in this transformation is that real innovation no longer emerges solely from the halls of traditional defence primes. It is taking shape in Munich garage laboratories, Berlin co-working spaces, and Hamburg deep tech incubators. A new generation of technology-driven companies positions itself as the bridge between the digital economy and security policy – and it is reshaping Europe’s entire innovation ecosystem.

1. The Rise of a New Defence-Tech Generation

In recent years, a new generation of Defence-Tech companies has emerged that differs fundamentally from traditional defence contractors. The contrast could hardly be starker: whilst classic defence programmes – such as the Tiger helicopter system or the Eurofighter – require decades of development and consume multi-billion-euro budgets, Defence-Tech start-ups are delivering operationally ready systems within twelve to twenty-four months.

They operate on the model of modern software companies: rapid iteration, data-driven product development, and a pronounced software component as the core of their value proposition.6

6 Bitkom e.V. (2026): DefTech Report 2026 – Defence and Dual-Use in Germany. Berlin: Bitkom.

The most prominent European example is Helsing. Founded in Munich in 2021, the company develops AI-powered software for military systems and has become Europe’s most valuable Defence-Tech company in just four years. Following a Series D funding round of over €600m in June 2025, Helsing is now valued at more than €12 billion – already qualifying it as a European decacorn.7 Helsing also acquired Bavarian aircraft manufacturer Grob Aircraft to develop its own drones and underwater systems – a move that signals its ambition to build a fully integrated defence technology platform.8

7 Helsing AI (2025): Series D Funding Round, June 2025. Available at: https://helsing.ai. Valuation per Munich Startup Insights (Feb. 2026): >€10bn.

8 Munich Startup (2026): Munich Unicorns 2026 – These unicorns will shape the startup scene. Februar 2026. Online: https://www.munich-startup.de

An equally steep trajectory has been followed by Quantum Systems, based in Gilching near Munich. Founded in 2015 by a former Bundeswehr pilot as an agricultural technology company, the start-up pivoted aggressively into the defence sector following Russia’s attack on Ukraine. In May 2025, Quantum Systems achieved unicorn status after a €160m funding round – led by Balderton Capital, with participation from Hensoldt, Airbus Defence and Space, and Peter Thiel.9 A further funding round at the end of 2025 pushed the valuation to over €3 billion. The company now produces up to 4,000 drones per annum for military customers in Germany, Ukraine, the United States, Spain, Australia, and New Zealand, and is targeting a stock market listing in 2026.

9 Munich Startup / TechFundingNews (2025): Quantum Systems becomes Germany’s first defense tech unicorn. Mai 2025; TFN November 2025.

Alongside these flagship companies, a broad ecosystem of further players is emerging: ARX Robotics develops autonomous ground vehicles, Alpine Eagle focuses on counter-drone systems, and Isar Aerospace is advancing commercial rocket propulsion. The Bitkom DefTech Report 2026 documents that DefTech and Dual-Use start-ups in Germany alone accounted for 17 % of total German venture capital – despite representing only around 2 % of all deals. In 2025, half of all new German unicorns originated from the Defence or Dual-Use sector.10

10 Bitkom e.V. (2026): DefTech Report 2026 – Defence and Dual-Use in Germany. Berlin: Bitkom.

2. Venture Capital Discovers Defence Technology

One of the most remarkable developments of recent years is the massive entry of venture capital into the Defence and Dual-Use sector. As recently as 2019, defence technology was widely regarded as uninvestable across much of the European VC community – not least because of rigid ESG exclusion clauses and the societal taboo that Germany’s historical legacy imposed on the sector. Today, that picture has been fundamentally and permanently transformed.11

11 Tech.eu (2025): Europe’s defencetech investment hits new highs. September 2025. Online: https://tech.eu

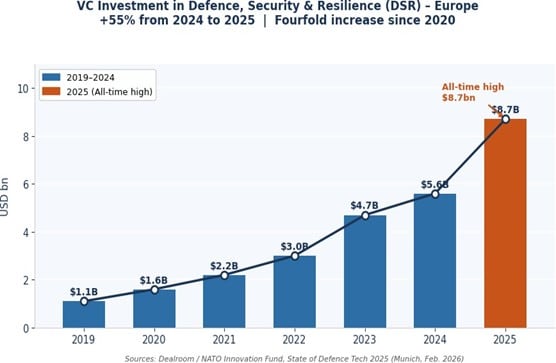

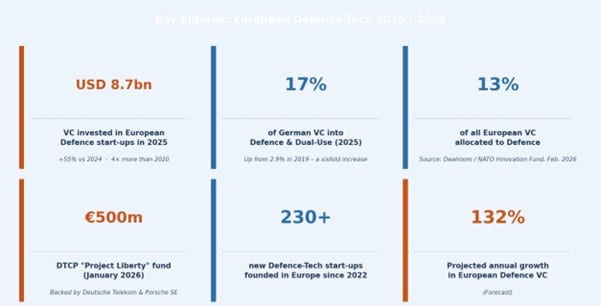

The latest data from the Dealroom/NATO Innovation Fund’s ‘State of Defence Tech 2025’ report, presented at the Munich Security Conference in February 2026, paints a clear picture: venture capital investment in European Defence, Security and Resilience (DSR) start-ups rose by 55 % in 2025 to a record high of $8.7bn. Compared to 2020, this represents a fourfold increase. The DSR sector now accounts for 13 % of all European venture capital investment – compared to 4 % in 2020.12 13

12 Dealroom.co / NATO Innovation Fund (2026): State of Defence, Security & Resilience Tech 2025. Report presented at the Munich Security Conference, February 2026.

13 Vestbee (2025): Europe raises record $1.5B for defence tech. Oktober 2025. Online: https://www.vestbee.com

Figure 1: VC Investment in Defence, Security & Resilience (DSR) – Europe 2019–2025 | Source: Dealroom / NATO Innovation Fund (Feb. 2026)

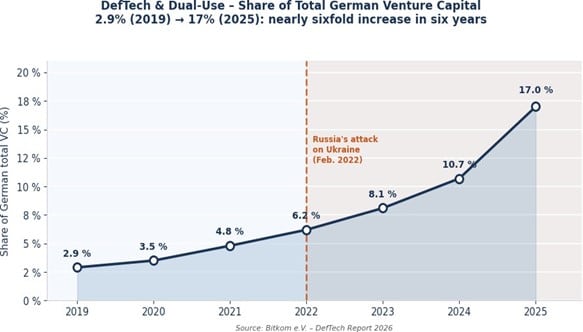

For the German market, the Bitkom DefTech Report 2026 shows an even sharper dynamic: the share of DefTech and Dual-Use in total German venture capital has risen from 2.9 % in 2019 to 17 % in 2025 – a more than sixfold increase in six years.14

14 Bitkom e.V. (2026): DefTech Report 2026 – Defence and Dual-Use in Germany. Berlin: Bitkom

Figure 2: DefTech & Dual-Use Share of Total German Venture Capital 2019–2025 | Source: Bitkom DefTech Report 2026

At the technology level, artificial intelligence dominates: in 2025, AI-based DSR systems absorbed 44 % of all European DSR investment – the highest share in six years. Quantum technologies (computing, cryptography, sensors) reached $2.4bn – 2.4 times more than in 2024.15

15 Dealroom.co / NATO Innovation Fund (2026): State of Defence, Security & Resilience Tech 2025. Report presented at the Munich Security Conference, February 2026.

In parallel, specialised fund vehicles are emerging that further institutionalise the sector. Hamburg-based investment manager DTCP closed the ‘Project Liberty’ fund with a volume of €500m in early 2026, backed by Deutsche Telekom and Porsche SE, and focused on European Defence and Dual-Use technology companies at Series A to C stage.16 The NATO Innovation Fund is investing $1 billion in European security start-ups. The European Investment Bank (EIB) has launched its InvestEU Defence Equity Facility and committed €50m to Join Capitals Fund III.17

16 EU-Startups (2026): DTCP raises EUR 500 million Project Liberty fund for European defence tech. Januar 2026. Online: https://www.eu-startups.com

17 European Commission / EIF (2026): InvestEU Defence Equity Facility – EIF commits €50m to Join Capital Fund III. March 2026. Available at: https://defence-industry-space.ec.europa.eu

Noteworthy is the geographical composition of capital: approximately 40 to 50 % of late-stage capital originates from US investors – a signal that the European Defence-Tech market is perceived as globally relevant, but also indicative of a structural dependence of European companies on foreign capital.18

18 Russell Investments (2025): Europe’s Defense Tech Awakens: Where to Invest. September 2025. Online: https://russellinvestments.com

3. Germany’s Defence Budget: The Zeitenwende in

Numbers

No other factor is driving the boom in European Defence-Tech as powerfully as the historic increase in defence budgets. Germany is at the forefront of a Europe-wide reorientation.

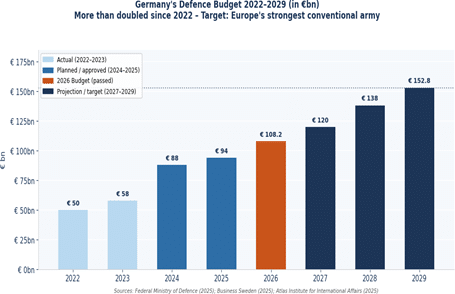

The figures are striking: Germany’s 2026 defence budget stands at €108.2 billion – compared to €50.3 billion in 2022, a doubling in just four years.19 Combined with the €100bn special fund, which will be fully disbursed by 2027, approximately €77 billion from the special fund flowed into the Bundeswehr between 2025 and 2027. Chancellor Friedrich Merz has set the objective of making Germany the ‘strongest conventional army in Europe’ and has charted a course towards the 3.5 % of GDP target by 2029.20

19 AtlasInstitute for International Affairs (2025): Germany’s Path to Kriegstüchtigkeit: The 2026 Defence Budget. Dezember 2025. Online: https://atlasinstitute.org

20 Atlantic Council (2025): Germany wants to double its defense spending. August 2025. Online: https://www.atlanticcouncil.org

Figure 3: Germany’s Defence Budget 2022–2029 in €bn | Sources: BMVg, Business Sweden (2025), Atlas

Institute (2025)

At NATO level, a new benchmark was agreed at the Hague Summit in June 2025: 5 % of GDP by 2035, comprising 3.5 % for core defence and 1.5 % for resilience and infrastructure. All 32 NATO members met the previous 2 % target for the first time in 2025.21 22 For context: as recently as 2023, only ten Allies were meeting this target.

21 PBS NewsHour / AP (2025): All NATO members projected to hit old spending target. August 2025. Online: https://www.pbs.org

22 CSIS (2025): Chapter 13 – Defense Budgets in an Uncertain Security Environment. Oktober 2025. Online: https://www.csis.org

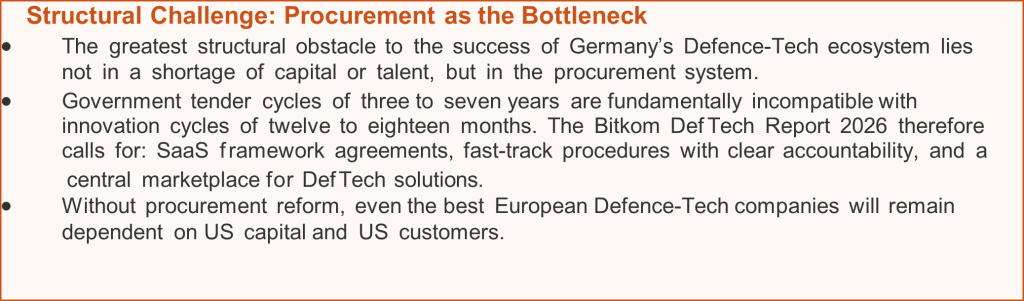

This budget transformation has direct implications for the innovation landscape: larger defence budgets do not merely represent greater procurement volume for traditional prime contractors; they also create, for the first time, reliable procurement pipelines for start-ups – one of the sector’s most significant historical bottlenecks. The Bitkom DefTech Report 2026 notes critically that 76 % of DefTech founders surveyed continue to regard Germany’s defence capabilities as weak despite the budget growth – in particular owing to the persistently slow procurement processes.23

23 Bitkom e.V. (2026): DefTech Report 2026 – Defence and Dual-Use in Germany. Berlin: Bitkom.

4. Munich as Epicentre: Europe’s Defence-Tech Capital

Within Europe, a clear geographical concentration has crystallised. According to Dealroom and the NATO Innovation Fund, Munich raised $1.7bn in 2025, making it Europe’s leading Defence-Tech hub – ahead of London and Cambridge (both $1.2bn), Helsinki ($576m), and Paris ($453m).24

24 Dealroom.co / NATO Innovation Fund (2026): State of Defence, Security & Resilience Tech 2025. Report presented at the Munich Security Conference, February 2026.

Munich’s locational advantages stem from a unique combination of factors: the Technical University of Munich (TUM) and the Bundeswehr University Munich provide a constant stream of highly qualified graduates. Industrial conglomerates such as Airbus Defence and Space, Hensoldt, KNDS, MBDA, MTU, and Rohde & Schwarz provide an industrial anchor. Specialist deep tech investors such as Alpine Space Ventures, Vsquared Ventures, Bayern Kapital, and DTCP supply the capital.25

25 xpert.digital (2025): Bavaria’s Defence and Dual-Use Ecosystem: Helsing, ARX Robotics & Co. Oktober 2025.

The result is an ecosystem that enables short pathways from research to application. Munich’s key companies, Helsing and Quantum Systems, are not isolated success stories but beacons that attract further talent and capital. As Munich Startup documents, Munich’s start-up scene held its own well in 2025 despite a constrained global VC market: 274 documented funding rounds, with a focus on deep tech, life sciences, and cybersecurity.26

26 Munich Startup (2025): That was 2025 – Year in Review. Dezember 2025. Online: https://www.munich – startup.de

Figure 4: Munich Technology Unicorns & Decacorns 2025/2026 by Valuation | Sources: Munich Startup (Feb. 2026), Dealroom, TFN (2025)

Alongside the private ecosystem, public funding plays an important role: Bavaria’s High-Tech Agenda is expanding research infrastructure, creating new professorships, and investing specifically in quantum computing infrastructure within the Munich Quantum Valley framework. The BMBF Security Research Framework Programme is providing approximately €580m by 2027. The EU has allocated a total of €7.9 billion under the European Defence Fund (EDF) for the period 2021 to 2027 for defence-related research and development.27

27 European Defence Fund (2024): Annual Report 2023/2024. Brussels: European Commission. (Total volume €7.9bn, 2021–2027)

5. The Role of Dual-Use Technologies

A decisive structural factor driving the sector’s growth dynamic is the dual-use character of core technologies. Artificial intelligence, robotics, satellite communications, cybersecurity, and autonomous systems are deployed in both civilian markets and military applications, thereby scaling within a substantially larger addressable market than purely military systems.28

28 McKinsey & Company (2024): The dual-use technology landscape: Opportunities and challenges. McKinsey Technology Report.

The strategic rationale of many companies is transparent: Quantum Systems began as an agricultural technology start-up before adapting its drone technology for military applications.

The core technology – AI-powered image processing, navigation systems, and autonomous control – is identical. What changes are hardening, certification requirements, and operational scenarios.

This approach offers several strategic advantages: the civilian market finances and accelerates underlying technological development. Faster innovation cycles driven by commercial demand enable continuous product improvement. Dependence on lengthy government procurement cycles is reduced. And best-in-class talent is more easily attracted when a company also has commercial relevance.

Nevertheless, there are critical limitations to this model: the EU Dual-Use Regulation and the German Foreign Trade and Payments Act (Außenwirtschaftsgesetz) create a complex regulatory framework that places considerable compliance burdens on start-ups. Rockaway Ventures investor Joachim Enegaard warned explicitly in February 2026 that ‘dual-use is being misused as a marketing label in many cases – and that autonomous systems and security protocols operate under fundamentally different rules than conventional software investing’.29

29 The Recursive / Rockaway Ventures (2026): Europe’s Defense Tech Investing Plays by Different Rules. Februar 2026. Online: https://therecursive.com

6. Technological Sovereignty as a Strategic National Objective

A further central driver is the political objective of Europe’s technological sovereignty. This concept embodies the strategic recognition that dependence on American or Asian technologies in sensitive areas – semiconductors, AI, satellite communications, cybersecurity – represents a systemic security risk.

The Russell Investments analysis of September 2025 identifies the core of the problem: 65 % of European Defence-Tech late-stage capital originates from US or Asian investors. Nearly half of all funding rounds exceeding $200m are dominated by non-European sources.30 In critical geopolitical situations, this capital dependency could prove to be a strategic vulnerability.

30 Russell Investments (2025): Europe’s Defense Tech Awakens: Where to Invest. September 2025. Online: https://russellinvestments.com

Accordingly, both the EU and the Federal Government have substantially expanded the development of independent Defence-Tech funding instruments: the EDF is providing €7.9 billion for European defence research. The EIB and EIF are mobilising private capital through the InvestEU Defence Equity Facility. NATO has established its own start-up support programme through DIANA (Defence Innovation Accelerator for the North Atlantic). Since 2022, more than 230 new Defence-Tech start-ups have emerged across Europe.31 32

31 European Commission / EIF (2026): InvestEU Defence Equity Facility – EIF commits €50m to Join Capital Fund III. March 2026. Available at: https://defence-industry-space.ec.europa.eu

32 Jerusalem Post (2025): Why Europe’s defence startups are booming in 2025. Online: https://www.jpost.com

7. Challenges and Risks

Alongside the obvious opportunities, the dynamics of the European Defence-Tech sector also present structural risks that warrant sober assessment.

Procurement Reform as the Critical Path

The greatest structural challenge remains public procurement. Even excellent technologies cannot fulfil their strategic purpose if they fail to reach operational deployment. The Bitkom DefTech Report 2026 urgently calls for fast-track procedures, SaaS framework agreements, and a central marketplace for DefTech solutions.33

33 Bitkom e.V. (2026): DefTech Report 2026 – Defence and Dual-Use in Germany. Berlin: Bitkom.

Capital Structure and Dependency

The dominance of US capital in European Defence-Tech late-stage financing is both symptom and cause: a symptom of an underdeveloped European late-stage financing landscape, and a cause of potential regulatory and strategic dependencies in the future.34

34 Russell Investments (2025): Europe’s Defense Tech Awakens: Where to Invest. September 2025. Online: https://russellinvestments.com

Ethics, ESG, and Social Acceptance

Despite the increased social acceptance of security investments, the ethical dimension remains a permanent concern. Many institutional investors – in particular pension funds and certain sovereign wealth funds – continue to be subject to restrictive ESG frameworks that limit or exclude Defence investments. This reduces the available capital pool and structurally increases the cost of capital for European Defence-Tech companies.

Conclusion

The transformation of the European Defence-Tech ecosystem entered a new phase in 2025/2026: from ‘emerging’ to ‘mainstream’. With $8.7bn of DSR investment in Europe, a 17 % share of the German VC market, and the rise of world-class companies such as Helsing and Quantum Systems, the sector is no longer a niche – it is structural.35

35 Dealroom.co / NATO Innovation Fund (2026): State of Defence, Security & Resilience Tech 2025. Report presented at the Munich Security Conference, February 2026.

Germany, and Munich in particular, has assumed a leadership position that should not be taken for granted. It is the result of industrial strength, excellent universities, and – crucially – a geopolitical shock that brought down ideological barriers. The question is no longer ‘whether’ Germany will have a Defence-Tech ecosystem, but ‘how well’ it will succeed in converting this momentum into a lasting, innovation-driven, and sovereign industrial foundation.

The critical bottleneck remains procurement: so long as start-ups develop excellent technologies but cannot get them into the hands of the Bundeswehr, the vast majority of the potential is wasted. The reforms of the next two to three years will determine whether Germany is merely a capital market for Defence-Tech – or a strategic technology location.